Introduction

Contact-less payments have transformed the way people shop and pay for everyday purchases. A simple tap of a card or mobile device can complete a transaction within seconds, offering customers speed and convenience. However, behind every tap is a complex payment processing system involving merchants, banks, payment networks, and advanced security technologies.

Understanding what happens after you tap your Mastercard can help businesses and consumers better appreciate the technology that enables fast, secure, and reliable payments.

Steps of Mastercard Payment Processing

Step 1: The Card or Device Sends Payment Information

When a customer taps a Mastercard on a contact-less payment terminal, the card or digital wallet communicates with the terminal using Near Field Communication (NFC) technology.

The payment device sends encrypted transaction information, including details required to verify the payment. Unlike traditional card payments, contactless transactions use secure communication methods designed to protect sensitive information.

If a customer uses a mobile wallet, such as a smart-phone or smart-watch, the device may use a digital token instead of the actual card number. This helps protect the customer’s payment details during the transaction.

Step 2: The Merchant’s Payment Terminal Processes the Request

Once the terminal receives the payment information, it creates a transaction request. This request includes important details such as:

- Transaction amount

- Merchant information

- Payment credentials

- Security data generated during the tap

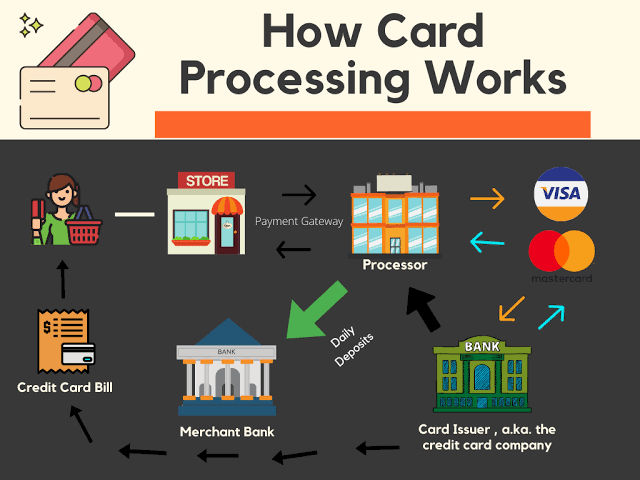

The merchant’s payment system then sends this information to the payment processor or acquiring bank. The acquiring bank is the financial institution that manages payment acceptance for the merchant.

Step 3: The Payment Network Routes the Transaction

After the acquiring bank receives the transaction request, it forwards the information through the Mastercard payment network.

Mastercard acts as the connection between the merchant’s bank and the customer’s card issuer. It does not issue cards directly but provides the technology and infrastructure that enable secure communication between financial institutions. During this stage, Mastercard helps route the transaction request to the correct issuing bank for approval.

Step 4: The Issuing Bank Verifies the Payment

The issuing bank is the financial institution that provided the Mastercard to the customer. When it receives the transaction request, it performs several security checks.

Advanced fraud prevention systems may analyse the transaction in real time to identify unusual activity. If everything meets security requirements, the issuing bank approves the payment.

Step 5: Transaction Approval Is Sent Back

Once the issuing bank approves the transaction, the approval message travels back through the Mastercard network to the acquiring bank and then to the merchant’s payment terminal. The customer sees confirmation on the screen, hears a payment notification, or receives a receipt. This entire process usually takes only a few seconds.

Step 6: Settlement and Fund Transfer

Although the payment is approved instantly, the actual transfer of funds happens during the settlement process.

The merchant’s bank receives funds from the customer’s issuing bank through the payment network. After processing fees are deducted, the remaining amount is transferred to the merchant’s account.

Conclusion

As digital payments continue to grow, Mastercard payment processing will remain an essential part of the global financial ecosystem. The next time you tap your card, remember that a secure network of technologies and financial institutions is working behind the scenes to complete your payment within seconds.